Toll roads are a key segment of the global infrastructure market. However, these assets also have some rather unique characteristics. This means that shorthand valuation measures/metrics (eg. P/E ratios and EV/EBITDA) can generate misleading outcomes.

Key characteristics that have an impact on valuing toll roads

The key characteristics to consider when valuing a toll road are outlined below:

Toll roads operate under a concession agreement (or contract) with a government that, among other things, sets out two critical factors:

- The date at which the concession agreement terminates; and

- The basis on which the tolls will increase.

When the concession actually terminates, the asset is handed back to the government, i.e. unlike most other enterprises, there is no terminal value.

Toll roads operate on relatively high EBITDA margins (EBITDA being revenue minus expenses before depreciation, interest and tax), typically around 80%-90% for urban toll roads and 70% for inter-urban roads. This means that for a typical urban toll road, only 10%-20% of revenue is used to operate and maintain the toll road.

Toll roads involve significant upfront build costs and the standard accounting treatment applied to toll roads is to amortise the capital costs of construction over the life of the concession to reflect expected maintenance or replacement expenditure. However, in the case of a road, maintenance is a relatively small proportion of revenue (say 2% p.a.), and is generally expensed rather than capitalised. This means that the depreciation entry for accounting purposes significantly overstates the actual expenditure needed to maintain the road. An example of this is Australian toll road company, Transurban, which incurred an accounting depreciation expense of A$550 million but had a cash maintenance cost of only A$55 million.

We believe that P/E ratios are meaningless when analysing toll roads. Not only is the cashflow generated by the business almost always higher than the published accounting earnings, but the ratio also ignores the fundamental nature of toll roads - that they are limited life assets.

For most normal industrial companies, depreciation is a good proxy for the maintenance costs needed to keep a business operating competitively. However, for toll roads, given the disparity between accounting depreciation and the real cost of maintaining toll roads, accounting earnings can significantly understate the underlying position of the business and the free cash it generates.

This disparity has another indirect benefit to the underlying value of the business. Accounting earnings are lower and hence so is the tax that the business will have to pay, thus actual post-tax cashflow is higher.

P/E is a proxy for the net present value of the cashflow from the earnings of a business, however for toll roads, the valuation needs to be based on the underlying free cashflow generation.

The Transurban-owned 495 Express Lanes represents a 22km (13.7 mile) stretch of high occupancy lanes and a key arterial connection in Northern Virginia, USA.

Is an EV to EBITDA multiple a good measure when valuing toll roads?

Another short hand measure often used when valuing normal industrial companies is the Enterprise Value (EV) to EBITDA ratio. In the examples that follow, each case uses a discounted cashflow methodology to value the toll road by forecasting cash flows under the assumptions set out below.1

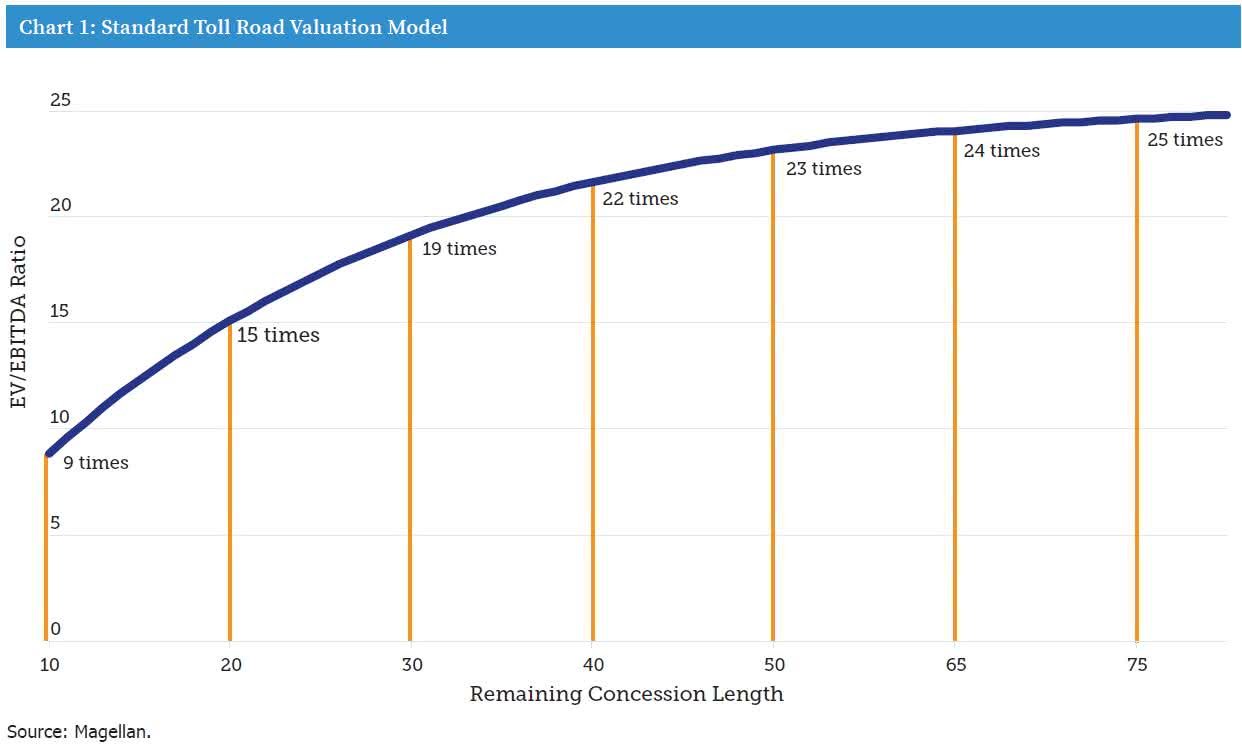

Chart 1 is based on a standard toll road model where the key assumptions are as follows:

Traffic in Year 1 grows at 2% with the growth rate reducing by 0.1% per annum.

The EBITDA margin is 75% in year 1, growing each year by 0.5% to a maximum 90%.

Tolls increase with inflation of 2% p.a.

As Chart 1 highlights, under this scenario the EV/EBITDA ratio appropriate to the valuation of this hypothetical toll road increases with the concession length, so a rational investor would value the toll road at 15 times current year EBITDA if there were only 20 years remaining on the concession but would be prepared to pay 22 times if there were 40 years remaining and almost 25 times if there were 70 years remaining.

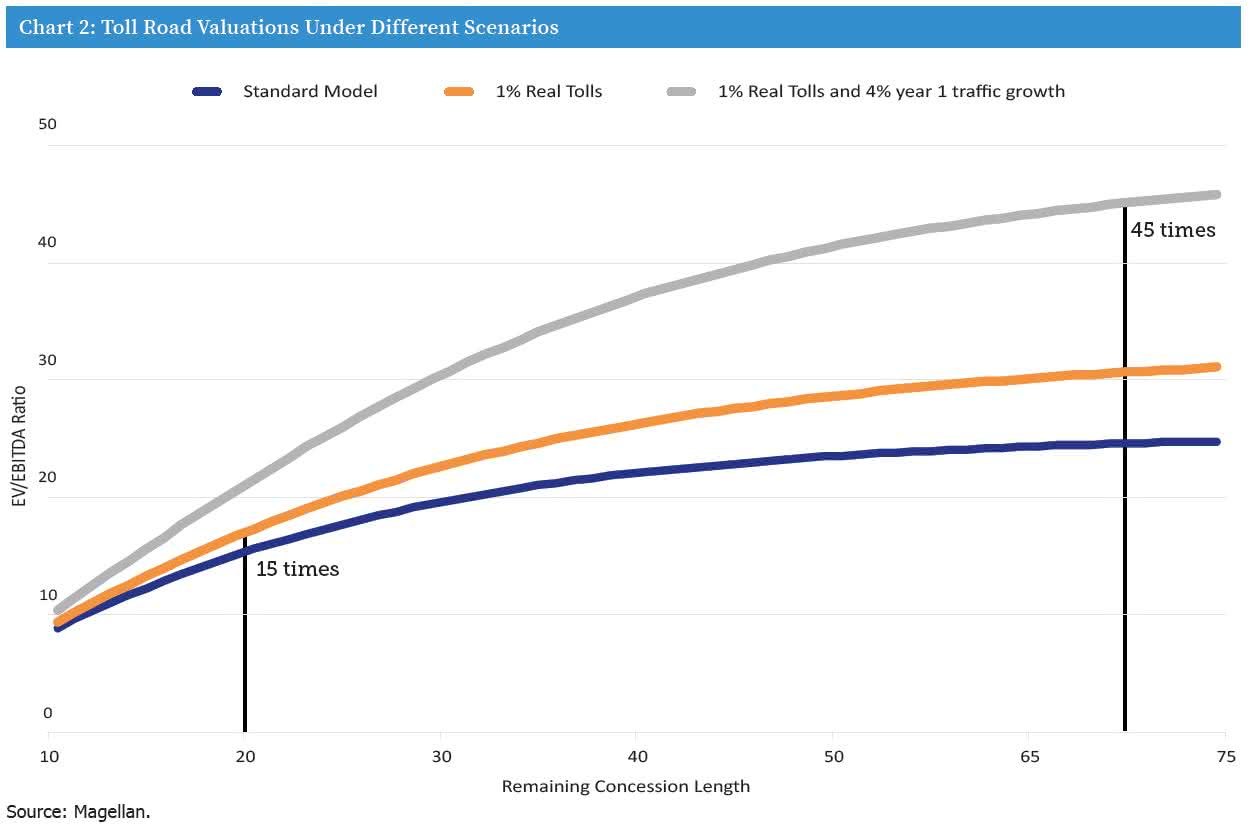

But concession length isn’t the only important variable in valuing a toll road. Given that toll roads have a largely fixed cost base, the rate of growth of revenues can clearly be a critical factor in a toll road’s value. Chart 2 shows the shape of the curve under two additional scenarios:

Scenario 2: As per the standard model shown in Chart 1 but with tolls increasing by 1% in real terms instead of in line with inflation; and

• Scenario 3: as per Scenario 2 but with traffic growth starting at 4% growth instead of 2% in year 1

(and also fading at 0.1% p.a).

1Valuing the future cash flows of the road using a Weighted Average Cost of Capital of 6.8% based on a nominal cost of equity of 7.0%, a nominal cost of debt of 6.0% and assuming 40% gearing. For simplicity the hypothetical toll road enterprise value is determined pre-tax and interest costs.

As Chart 2 highlights, a rational investor would be prepared to pay approximately 15 times EBITDA for a standard toll road with 20 years remaining in the concession period but as high as 45 times Year 1 EBITDA if it was a scenario 3 toll road with 70 years remaining on the concession.

Every aspect of the toll road’s earnings in the three scenarios in Year 1 is identical, i.e. they all have the same revenue, EBITDA and earnings. Yet the actual NPV of each asset’s future cash flows varies enormously.

Thus EV/EBITDA is also not useful for valuing and comparing toll roads as a fair multiple will be determined by the length of the concession, expected traffic and price growth, none of which are reflected in the current EBITDA of the toll road under analysis.

Concluding comments

Any use of current year financial results such as P/E or EV/EBITDA ratios as a means to determine the value of a toll road is problematic at best and most likely misleading. The corollary is that there is only one way to effectively value a toll road business – value each asset over its entire concession period and aggregate the sum of those assets. On that basis, our analysis suggests that a number of the world’s highest quality toll roads remain attractively priced.

Important Information: This material has been produced by Magellan Asset Management Limited trading as MFG Asset Management (‘MFG Asset Management’) and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision.

This material may include data, research and other information from third party sources. MFG Asset Management makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of MFG Asset Management. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon.

Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of MFG Asset Management.

By clicking “I Agree” you represent that you are a ‘wholesale client’ under section 761G of the Corporations Act 2001 (Cth) (the “Act”). Further, you represent that you will not directly or indirectly disseminate information contained on this website to a ‘retail client’ within the meaning of section 761G of the Act.

This website contains general information only and does not take into account any person’s investment objectives, financial situation or needs. Nothing contained in the website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: The information contained in the Institutional section of this website is not intended to constitute:

any offer for sale or subscription of securities to the public in New Zealand in terms of the Securities Act 1978 of New Zealand (the 1978 Act) (or any statutory modification or re-enactment of, or statutory substitution for, the 1978 Act). Accordingly, no prospectus or investment statement for the purposes of the 1978 Act has been produced in respect of the information contained in the website and the information does not contain all the information typically included in a registered prospectus or an investment statement under the 1978 Act; or

the provision of "financial advice" under the Financial Advisers Act 2008 (the 2008 Act) (or any statutory modification or re-enactment of, or statutory substitution for, the 1978 Act).

By clicking "I agree," you agree that you have read the terms detailed below and confirm that:

1) you:

(i) are an "habitual investor" for the purposes of section 3(2)(a)(ii) of the 1978 Act. "Habitual investors" are persons whose principal business is the investment of money or who, in the course of and for the purposes of their business, habitually invest money; or

(ii) otherwise fall within one of the other categories set out in section 3(2)(a) of the 1978 Act, meaning that you are not a member of the public for the purposes of the 1978 Act; or

(iii) you are acting for a person described in (i) or (ii); and

2) you are a "wholesale client" for the purposes of the 2008 Act.

The information contained in the Institutional section of this website is intended only for institutions that are both (i) habitual investors or otherwise fall within one of the other categories set out in section 3(2)(a) of the 1978 Act and (ii) "wholesale clients" under the 2008 Act. Such persons shall be referred to as "institutional investors" herein. Persons who are not institutional investors should not review the information contained in the website. This website is supplied on the condition that it is not passed on to any person who is not an institutional investor.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an Institutional Investor and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorised.

The information is intended for institutional investors and consultants to institutional investors and is published for informational purposes only. The information is directed at informing persons falling within one or more of the following categories:

1) A government, local authority, or public authority;

2) A bank or insurance company;

3) A pension fund or charity;

4) An individual who is a "qualified client" under the Investment Advisers Act of 1940 and has experience in investment, financial and business matters to evaluate the risks of investing in securities;

5) Persons whose ordinary activities involve or are reasonably expect to involve them, as principal or as agent, in acquiring, holding, managing or disposing of investments for the purpose of a business carried on by them;

6) Persons whose ordinary business involves the giving of advice, which may lead to another person acquiring or disposing of an investment or refraining from so doing.

Persons who do not fall into one of the above categories should not review the information contained in this site.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an investment professional as that term is defined in the Handbook of the Financial Conduct Authority ("FCA") or that I am acting for an investment professional.

Information contained on the Institutional section of this website is not intended for investors in any jurisdiction in which distribution of the information or purchase is not authorized or permitted.

The information is exclusively intended for, and directed at, investment professionals and advisers to investment professionals. Any products and investment services that are referenced on this website are only available to, or will only be engaged in with, investment professionals. Investment professionals will usually fall within one or more of the following categories (terms used have the same meaning as in the FSA handbook):

1) An authorised person;

2) An exempt person;

3) A government, local authority (constituted in any jurisdiction) or an international organisation;

4) Any person whose ordinary activities involve him in carrying on an investment activity;

5) A person who is acting in their capacity as a director, officer or employee of the above.

Persons who do not fall into one of the above categories, or who do not otherwise constitute investment professionals, should not read or rely on the information contained on this website.

The information provided on this website is for information purposes only and nothing on this website constitutes investment, legal, business, tax or any other type of advice.

Any performance data shown represents past performance. Past Performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the risks associated with investments generally and the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Accredited Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for accredited investors in any jurisdiction in which distribution or purchase is not authorized.

The information is intended for accredited investors and consultants to accredited investors, and is published for informational purposes only.

The term "Accredited Investor" is a defined term under the Canadian Securities Regulation and includes Institutional Investors, such as banks, insurance companies, trust and loan companies, and pension plans. It also includes individuals provided they meet certain net worth or income thresholds. For more information, refer to National Instrument 45-106 of the Canadian Securities Administrators or consult your legal adviser.

Persons who do not fall into the definition above should not review the information contained in the site.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Institutional Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is exclusively intended for, and directed at eligible counterparties or professional clients as defined under the German Securities Trading Act. For more information, consult your legal adviser.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Institutional Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is intended for institutional investors and consultants to institutional investors, and is published for informational purposes only. The information is directed at non-retail clients falling within one or more of the following categories:

1) A government, local authority or public authority;

2) A bank or insurance company;

3) A pension fund or charity;

4) An individual who provides one or more investment services on a professional basis;

5) Persons whose ordinary activities involve or are reasonably expect to involve them, as principal or as agent, in acquiring, holding, managing or disposing of investments for the purposes of a business carried on by them;

6) Persons whose ordinary business involves the giving of advice, which may lead to another person acquiring or disposing of an investment or refraining from so doing.

Persons who do not fall into one of the above categories should not review the information contained in the site.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am an "Institutional Investor" and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is exclusively intended for, and directed at institutional investors, accredited investors and expert investors as defined under the Securities and Futures Act (Singapore) (“SFA”) For more information, refer to the SFA or consult your legal adviser.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Important Legal Information: By clicking "I agree," the user agrees that I have read the terms detailed below and confirm that I am a "professional investor" as defined under the Securities and Futures Ordinance of Hong Kong (the “Ordinance”) and any rules made under the Ordinance, and that I wish to proceed.

Information contained in the Institutional section of this website is not intended for institutional investors in any jurisdiction in which distribution or purchase is not authorized.

The information is exclusively intended for, and directed at, professional investors as defined under the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance. For more information, refer to the Securities and Futures Commission of Hong Kong or consult your legal adviser.

Nothing on this website constitutes investment, legal, business, tax or any other type of advice. The information on this website does not take into account the particular financial and investment objectives, circumstances and needs of any person. Information on the website is not intended for investors in any jurisdiction in which distribution or purchase is not authorized.

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your investment, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. Investors should be aware of the increased risks associated with investments in foreign/emerging markets securities, high yield securities and smaller companies.

You are solely responsible for evaluating the risks and merits regarding the use of the website and any services provided within. Nothing contained in that website constitutes a solicitation, recommendation, endorsement or offer to buy or sell any securities or other financial instruments.

Thank you for your interest. We are committed to expanding our institutional website to meet the needs of our global investor base. We do not, however, have content approved for your location at this time. For additional information please email institutional@magellangroup.com.au

Important Information

This document does not constitute an offer of units in a Magellan Fund in any jurisdiction other than Australia or New Zealand (or in jurisdictions where it is lawful to make such an offer). Applications for units in a Magellan Fund from residents outside of Australia and New Zealand may not be accepted.

By clicking on the "I Confirm" button below you are confirming that you are a resident of Australia or New Zealand (or that you are acting on behalf of a person who is a resident in one of those jurisdictions).

This means that the depreciation entry for accounting purposes significantly overstates the actual expenditure needed to maintain the road. An example of this is Australian toll road company, Transurban, which incurred an accounting depreciation expense of A$550 million but had a cash maintenance cost of only A$55 million.

This means that the depreciation entry for accounting purposes significantly overstates the actual expenditure needed to maintain the road. An example of this is Australian toll road company, Transurban, which incurred an accounting depreciation expense of A$550 million but had a cash maintenance cost of only A$55 million.