The energy crisis is likely to last years

September 2022

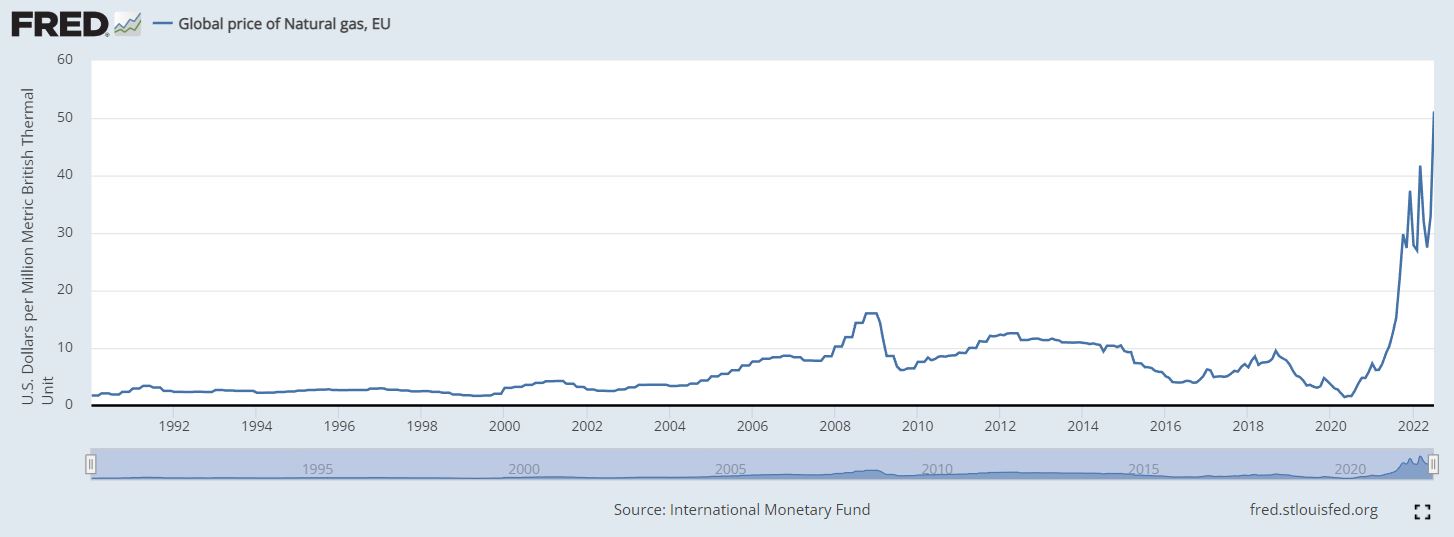

Europe is restarting mothballed coal-based power plants because the benchmark electricity price has exceeded 1,000% above its average of the past decade (where prices are set by the marginal cost of the last unit – essentially, the most expensive unit – of energy purchased to balance demand).[1] Electricity prices are spiralling because the cost of natural gas, the marginal fuel in most European electricity markets, has soared 1,300% above its decade average – the shock would be like oil nearing US$550 a barrel. The EU, in response, is imposing wartime-like price controls, rationing and a windfall tax on energy companies.[2] In the UK, the prospect of household energy bills jumping by 9 percentage points of GDP[3] has prompted London to announce emergency measures that, at an estimated cost of 150 billion pounds, is double the cost of the pandemic furlough scheme, and to reallow shale-gas fracking.[4] Norway, where hydropower generates 90% of local needs, may curb the export of electricity,[5] raising concerns cross-border flows could drop, even collapse, across Europe. French nuclear power output is diving due to maintenance and repairs – Électricité de France is only operating 26 of the country’s 57 reactors.[6] President Emmanuel Macron, who is fully nationalising the troubled nuclear operator, warns of the “end of abundance”.[7] Germany is worried that rage over energy prices driving inflation to near-50-year highs could turn violent.[8] Kosovo is facing two-hour blackouts every six hours, the first European country to display this feature of a failed state.[9] In China, daily hydro generation from the Three Gorges dam on the Yangtze River has dived 51%. Factories have suspended operations and cities are dimming lights.[10] Japan is overcoming its Fukushima fears and returning to nuclear power. Southeast Asia is using coal to replace the liquified natural gas diverted to Europe. South Asia is suffering blackouts because energy is unaffordable. US natural gas prices in August breached US$10 per million BTU, a 400% increase on the recent years, due to demand from Europe.

The first challenge is the unfavourable state of global politics. Europe’s torment is due to the significant cuts to the supply of Russian oil and natural gas that accounted for 40% of its energy needs. Moscow has weaponised gas supplies to inflict economic pain on Europe to undermine public support for arming Ukraine, while the West is seeking to restrict Russian oil sales. Oil and gas prices are likely to stay elevated in the near term because the world’s energy system cannot quickly replace Russia’s lost hydrocarbons, which equate to about 10% of global energy production.[11]

The Middle East is another concern. The return of Iranian oil to world markets could help Europe overcome the loss of Russian crude. But this depends on restoring the agreement on Iran’s nuclear capabilities between Iran and the EU, Germany and the five permanent members of the UN Security Council – one of which is Iran’s ally, Russia.[12] Moscow could easily delay any new agreement or ensure that any restored pact is short-lived.

The second big challenge for energy markets relates to climate change. Droughts and heatwaves in China, Europe and North America are hampering hydropower electricity generation (China, Italy, Norway, Spain and Portugal) while boosting demand beyond capacity to cope (the US). France’s nuclear-based EDF has cut production because receding rivers make it harder to cool reactors. Another angle to climate change is that renewable energy generation has not reached a level whereby it can compensate for Russia’s lost fossil fuels, hence the return to coal in Europe. Prior to the Ukraine war, Europe already had depleted energy storage due to a less-windy-than-usual weather idling wind farms, a problem worsened by Russia’s Gazprom withholding gas above contracted amounts, contrary to normal practice, ahead of the Ukraine invasion.[13]

The third challenge for energy markets is overcoming policymaker mistakes. The biggest error is that Europe, notably Germany, became overly dependent on Russian energy, especially natural gas that is not as easy as coal or oil to replace. A second mistake is France has failed to keep operational the country’s nuclear reactors that were mostly built in the 1980s and typically supply 70% of the country’s power needs.[14] A third error, many would argue, is the world’s turn away from nuclear energy after the Fukushima disaster in 2011. Many would say that a fourth blunder was not investing enough in renewables.[15] Plenty of blame will flow if the rising prices that are creating huge paper losses for utilities on Europe’s energy derivatives markets spark financial instability.[16] Governments, aware of the risk, have acted to ensure energy companies can meet collateral obligations.

Today’s energy crisis is still unfolding. The crisis-magnifying characteristics of energy markets – that inelastic demand maximises price increases when supply is troubled – give entrepreneurs the incentive to remedy these shortages. In time, the promise of profit will calm the energy crisis with clean solutions that snap Western dependence on despots. In the meantime, however, the disruption to French nuclear power, European hydropower and Russian gas and higher oil prices could cut global living standards, boost inflation, trigger a recession or worse in Europe, hound those in power, widen inequality within and between countries, trigger social unrest, spark industrial conflict and impede the fight against climate change. The damage inflicted just in Europe will likely make the 2020s energy crisis worse than that of the 1970s.

To be sure, this is a crisis centred in Europe and favourable developments in relation to the Ukraine war could calm things. Droughts will break and heatwaves pass. Maybe a sunny, warm and windy winter in Europe and energy substitution and conservation[17] will ease power costs. Efforts are underway to fill gas storage facilities across Europe – but, even at capacity, storage is a fraction of normal winter demand. Countries with gas and other energy reserves such as Algeria, Australia, Qatar and the US stand to gain. The recent fall in oil prices relieves some inflationary pressure.[18] But spot oil prices have declined on China’s pandemic lockdowns and concerns about a European recession.

The energy crisis largely created by Russia’s missing fossil fuels might best be viewed as shorthand for a series of crises around climate change, government finances, inequality, inflation, politics and social cohesion as well. Policymakers have much to solve before European gas and oil prices drop to anywhere near their pre-crisis averages.

The blind spot

In 2001, Russian President Vladimir Putin addressed the German parliament and in flawless German expressed a desire for warmer ties with the West. “Russia is a friendly European nation,” Putin declared.

German lawmakers leapt up in applause. One biographer of Angela Merkel wonders: Did Putin notice that in the second row of the Bundestag chamber, an unsmiling future chancellor who grew up in East Germany and spoke Russian remained seated? Merkel barely clapped. She knew KGB “values, loyalties and training are not so easily shed”.[19]

In 2020, Russian opposition leader Alexei Navalny collapsed after being poisoned with a nerve agent. He survived only because Merkel arranged for Navalny to be medivacked to Berlin. But even as Navalny lay in a coma in the Charité hospital, Merkel refused to cancel the Nord Stream 2 pipeline that would double the amount of gas pumped from Russia across the Baltic Sea to Germany.[20] Nord Stream 1, which has operated since 2011, carries 55 billion m3 of gas a year.

Merkel’s willingness to allow Germany to become dependent on Russian gas is now regarded as her blind spot. “Every time Obama asked Merkel why she was going ahead with Nord Stream 2, Merkel gave a different answer,” a national security adviser to the US administration of Barack Obama recalls.[21]

Other German policymakers were just as short-sighted. German Foreign Minister Heiko Maas and others in the German delegation smirked when Donald Trump in 2018 warned Germany it would become “totally dependent on Russian energy if it does not immediately change course”.[22] The German laughter reflected the country’s desire to reduce reliance on coal to mitigate climate change, eradicate nuclear power plants for safety reasons, save money, and a hope that greater economic ties would improve political ties with Russia.

Russia’s invasion of Ukraine prompted Germany to block Nord Stream 2. In retaliation, Russia is stifling flows through Nord Stream 1 and Europe is turning to LNG and other fossil fuels.

In time, the investment underway in renewables will be a big part of how Europe escapes the folly of relying on a non-renewable fossil fuel under the stranglehold of a hostile autocrat. Once Europe has secured affordable and clean energy, it will be able to close for good those coal plants being refired to overcome today’s energy emergency.

By Michael Collins, Investment Specialist

Global price of natural gas, EU

[1] Europe adopted this marginal-cost policy to prod investment in renewables. The marginal cost of wind and sun creating more power is theoretically close to zero while the marginal cost for fossil-fuel-based production is the cost of the coal or gas. See Yanis Varoukakis, former Greek minister of finance. ‘Time to blow up electricity markets.’ Project Syndicate. 29 August 2022. project-syndicate.org/commentary/marginal-cost-pricing-for-electricity-disastrous-in-europe-by-yanis-varoufakis-2022-08

[2] European Commission. ‘2022 state of the union address by President von der Leyen.’ 14 September 2022. ec.europa.eu/commission/presscorner/detail/ov/SPEECH_22_5493

[3] Carbon Brief, UK website focused on climate change. ‘Analysis: Why UK energy bills are soaring to record highs – and how to cut them.’ 12 August 2022. Household energy bills could rise from 4.5% of UK GDP in 2020 to 13.4% of output by next April. Household energy bills include energy spending on homes and cars. carbonbrief.org/analysis-why-uk-energy-bills-are-soaring-to-record-highs-and-how-to-cut-them/

[4] UK Prime Minister’s Office. ‘PM Liz Truss’s opening speech on the energy policy debate.’ 8 September 2022. Renewable and nuclear generators will move onto contracts for difference to end the situation where electricity prices are set by the marginal price of gas. gov.uk/government/speeches/pm-liz-trusss-opening-speech-on-the-energy-policy-debate

[5] The grid operators of Denmark, Finland and Sweden condemned the move in what should be a border-less market. ‘Nordic cooperation – More needed than ever to ensure electricity supply.’ Energinet. 19 August 2022. en.energinet.dk/About-our-news/News/2022/08/19/Nordic-cooperation-more-needed-than-ever-to-ensure-electricity-supply

[6] Javier Blas. ‘Paris faces an even colder, darker winter than Berlin.’ Bloomberg News. 29 July 2022. bloomberg.com/opinion/articles/2022-07-29/european-energy-crisis-paris-may-be-first-to-suffer-blackouts-this-winter

[7] ‘Macron warns of ‘end of abundance’ as France faces difficult winter.’ The Guardian. 25 August 2022. theguardian.com/world/2022/aug/24/macron-warns-of-end-of-abundance-as-france-faces-difficult-winter. /

[8] See World in depth. ‘Extremists plan ‘autumn of rage’ to exploit cost of living crisis in Germany.’ The Times. 25 August 2022. thetimes.co.uk/article/extremists-plan-autumn-of-rage-to-exploit-cost-of-living-crisis-in-germany-ht6sm5hbc. German inflation reached 8.8% in the year to August.

[9] Andrea Dudik. ‘A corner of Europe starts living with blackouts again.’ Bloomberg News. 26 August 2022. bloomberg.com/news/articles/2022-08-26/europe-energy-crisis-kosovo-learns-to-live-with-rolling-power-blackouts-again

[10] Bloomberg News. ‘Power crunch in Sichuan adds to industry’s woes in China.’ 21 August 2022. bloomberg.com/news/articles/2022-08-21/power-crunch-in-sichuan-adds-to-manufacturers-woes-in-china2

[11] International Energy Agency. ‘Energy fact sheet: Why does Russian oil and gas matter?’ 21 March 2022. iea.org/articles/energy-fact-sheet-why-does-russian-oil-and-gas-matter

[12] The Joint Comprehensive Plan of Action of 2015 that restricts Iran’s ability to develop nuclear weapons collapsed when the US withdrew in 2018.

[13] Russia refused to supply extra gas to Europe to make up for the shortage of wind-driven power. The speculation is the Kremlin instructed Gazprom not to supply extra gas in anticipation it would be weaponising gas after it invaded Ukraine.

[14] The industry failed to invest to sustain the reactors and failed to maintain its engineering expertise. See ‘French nuclear power crisis frustrates Europe’s push to quit Russian energy.’ The New York Times. 18 June 2022. nytimes.com/2022/06/18/business/france-nuclear-power-russia.html

[15] See Fatih Birol, executive director of the International Energy Agency. ‘Three myths about the global energy crisis.’ Financial Times. 6 September 2022. ft.com/content/2c133867-7a89-44d0-9594-cab919492777

[16] See ‘’Lehman event’ looms for Europe as energy companies face $1.5T in margin calls.’ Oilprice.com. 6 September 2022. See also The Economist, Free Exchange ‘Europe’s energy market was not built for this crisis.’ 8 September 2022. economist.com/finance-and-economics/2022/09/08/europes-energy-market-was-not-built-for-this-crisis

[17] See Chris Giles. ‘Europe can withstand a winter recession.’ Financial Times. 10 August 2022. ft.com/content/c9ec6d9d-a015-402c-a06e-f61b6ad87f92

[18] The US plan to impose a price cap on Russian oil shipments is prompting Russian oil companies to offer discounts on long-term contracts. See Julian Lee. ‘Russian oil producers feel the heat’ Bloomberg News. 25 August 2022. bloomberg.com/opinion/articles/2022-08-25/russian-oil-producers-feel-the-heat-elements-by-julian-lee

[19] Kati Marton. ‘The chancellor. The remarkable odyssey of Angela Merkel.’ William Collins 2021. Paperback. Page 108.

[20] Marton. Op cit. Pages 112 to 113.

[21] Marton. Op cit. Pages 113 to 114.

[22] ‘Trump accused Germany of becoming ‘totally dependent’ on Russian energy at the UN. The Germans just smirked.’ The Washington Post. 25 September 2018. washingtonpost.com/world/2018/09/25/trump-accused-germany-becoming-totally-dependent-russian-energy-un-germans-just-smirked/

Important Information: This material has been produced by Magellan Asset Management Limited trading as MFG Asset Management (‘MFG Asset Management’) and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision.

This material may include data, research and other information from third party sources. MFG Asset Management makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of MFG Asset Management. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon.

Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of MFG Asset Management.